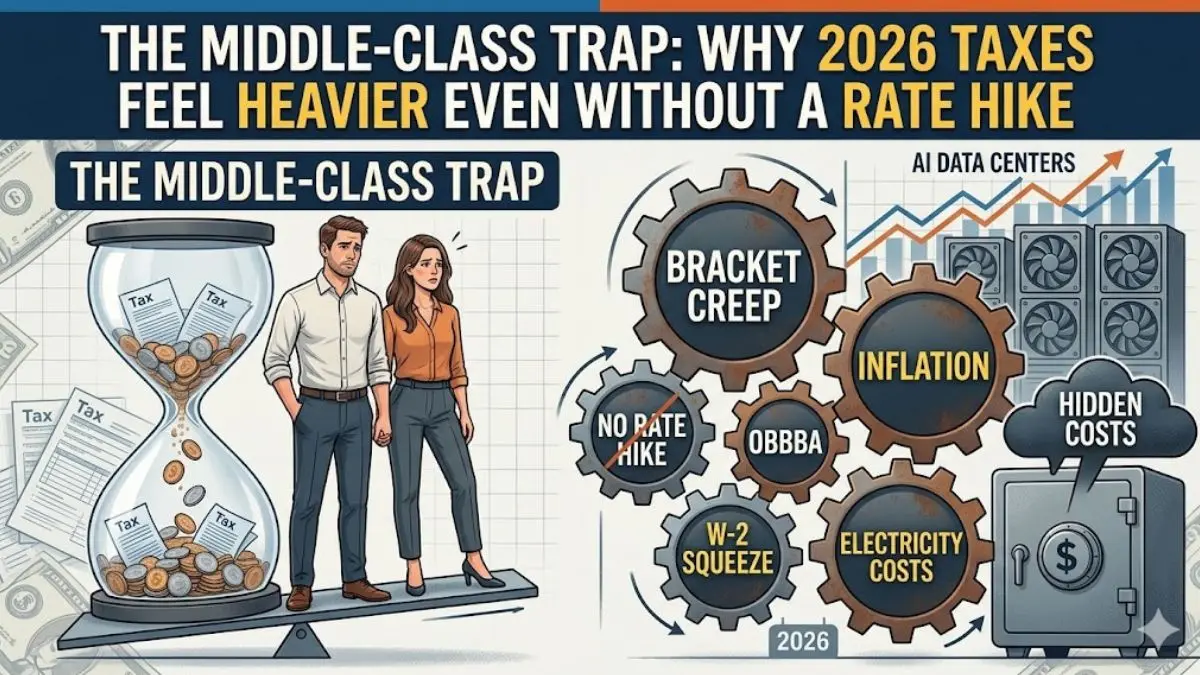

The Middle-Class Trap: Why 2026 Taxes Feel Heavier Even Without a Rate Hike

“I pay my taxes, I work harder every year — and somehow I end up with less.”

That’s the sentence many doctors, engineers, and small business owners are saying heading into 2026. The numbers partly back them up.

The One Big Beautiful Bill Didn’t Fix Everything

On July 4, 2025, President Trump signed the One Big Beautiful Bill Act (OBBBA) into law as Public Law 119-21. It prevented a major tax increase by making most expiring 2017 TCJA provisions permanent. Tax Foundation analysis shows the law increases average after-tax incomes by about 5.4% in 2026 relative to prior law, with meaningful benefits for many middle-income households on paper.

So why do so many middle-class families still feel financially strained? The answer is a three-part trap: structural differences in how labor versus capital income is taxed, cost-of-living pressures that often exceed official inflation adjustments, and rising electricity costs in regions with heavy AI data center growth. Understanding these helps clarify the disconnect.

Part 1 — Work vs. Wealth: The Divide That the OBBBA Didn’t Touch

Not all income is taxed equally — it’s written into the tax code. Wages face ordinary income rates plus payroll taxes. Long-term capital gains and qualified dividends receive preferential rates.

2026 Tax Comparison: The Professional vs. The Investor

| Feature | W-2 Professional (Middle Class) | High-Net-Worth Investor |

|---|---|---|

| Primary Income Source | Salary, bonuses, commissions | Long-term capital gains, qualified dividends |

| Federal Tax Type | Ordinary income + payroll taxes | Preferential capital gains rates |

| Top Marginal Federal Rate | Up to 37% | Capped at 20% (+ possible 3.8% NIIT) |

| Payroll Taxes (FICA) | 7.65% employee share on wages | Generally exempt on investment income |

| Typical Effective Rate Range | 15–28% after deductions | Often 12–23% with planning |

| Key Planning Tools | 401(k), HSA, standard deduction | Step-up basis, borrowing against assets, trusts |

The OBBBA kept the seven brackets (10%–37%) permanent and preserved preferential long-term capital gains rates (0%, 15%, 20%). For many married W-2 couples earning around $180,000, this often means the 22% or 24% marginal rate plus FICA. An investor with similar income from qualified dividends may face 15% with no FICA. This structural difference remains unchanged.

Part 2 — The Silent Squeeze: Inflation, Brackets, and the Purchasing Power Illusion

2026 Standard Deduction (Official IRS Figures)

- Single: $16,100

- Married filing jointly: $32,200

- Head of household: $24,150

Bracket thresholds rose roughly 2.3–2.7% (with extra adjustment for lower brackets under OBBBA). These changes largely prevent classic bracket creep from nominal raises alone.

In practice, many households still lose ground because real costs — housing, healthcare, groceries, and electricity — have risen faster than official CPI and wage growth in numerous regions. A 4% raise may not fully offset actual spending increases, creating a purchasing power gap even when tax brackets stay stable after indexing.

Part 3 — The Bill You Never Expected: AI Data Centers and Your Electricity Costs

Rising electricity bills in data-center-heavy areas surprise many families and have sparked policy debates nationwide.

Key Trends U.S. residential electricity prices have climbed steadily (national average in the 17–18 cents/kWh range recently, per EIA data). In regions like Northern Virginia (world’s largest data center cluster) and parts of PJM and ERCOT, load growth from AI/data centers contributes to higher wholesale prices and grid investment needs. Projections show significant U.S. data center demand growth — potentially doubling or more in coming years.

Real impacts vary: some residents in Virginia and PJM areas report noticeable bill increases, with surveys showing public concern. Utilities have sought large rate adjustments, and states are responding with new large-load rate classes, cost-allocation rules, and requirements for data centers to fund more infrastructure.

The debate is nuanced — data centers can bring jobs, tax revenue, and stable demand that may help spread costs long-term in some markets. In constrained grids, however, residential ratepayers can feel short-term pressure. This cost does not appear on your 1040 but functions as a higher living expense, hitting hardest where supply is tight.

What the OBBBA Did Get Right: New Benefits to Claim

The bill includes useful targeted relief (most temporary through 2028):

- Senior Bonus Deduction — Additional $6,000 per qualifying person 65+ (phases out at higher MAGI).

- No Tax on Tips — Deduction up to $25,000 (phases out above $150k/$300k MAGI).

- No Tax on Overtime — Deduction for premium portion up to $12,500/$25,000 (phases out similarly).

- New Auto Loan Interest Deduction — Up to $10,000 on qualifying new vehicles (phases out).

- SALT Cap — Temporarily raised to $40,000 (with modest annual increases through 2029, phaseouts apply).

- Expanded Child Tax Credit — To $2,200 per child.

- Trump Accounts for Children — New savings vehicles with contribution limits and seed money for some newborns.

- Above-the-Line Charitable Deduction — $1,000/$2,000 for non-itemizers.

Proven Tax Strategies That Still Work in 2026

- Max Your HSA — Triple tax advantage if eligible.

- Backdoor Roth IRA — Still viable for higher earners.

- Tax-Loss Harvesting — Offset up to $3,000 ordinary income.

- Review Itemizing vs. Standard Deduction — Especially with higher SALT cap.

- Employer Childcare Benefits — Expanded credits may support new programs.

The Barbell Economy: Who Actually Wins in 2026

Analyses describe a mixed distributional effect: strong benefits for many middle- and upper-middle households via rate stability and new deductions, plus targeted relief for tipped/overtime workers and seniors. Lower-income filers with minimal liability see smaller gains, while very high earners face phaseouts and other limits. The broad middle — especially W-2 earners without tips or high itemized deductions — experiences stability but not full relief from broader cost pressures.

Conclusion

Middle-class financial pressure in 2026 is real. It arises from embedded differences in labor vs. capital taxation, cost increases that outpace some official adjustments, and localized utility impacts from AI/data center growth.

The OBBBA delivered important stability and targeted breaks, but deeper structural and economic realities remain. Claim every eligible deduction, maximize HSAs and retirement accounts, review your SALT situation, and monitor local utility policies.

What pressures are hitting your household hardest in 2026? Share below — and consult a qualified CPA for personalized advice.